Transaction-Definition, Features, Classification, and Examples [Notes with PDF]

In this article, we will learn in-depth about transactions, including their definition, features, reasons, classification, identification method, and much more.

What is Transaction?

The transaction is very important for the recording of accounts, since the beginning of civilization, people have been trading with one another.

In ancient times, people exchanged goods between themselves to meet their needs, and since then the concept of transactions has arisen.

There is an event behind each transaction. That is, a transaction is the result of an event.

For example, a table purchased for the office with $5,000 and paid the child’s school fees $200. Both these incidents are events and each of which is measurable in terms of money and also has changed the financial position.

So, in simple terms, we can say that a transaction that is measurable in terms of money and changes in the financial position of a person or organization is to be treated as a transaction.

8 Important Features of Transaction

Which events will be considered transactions and which events will not be considered transactions, are measured by analyzing the characteristics of the transaction.

The 8 important features of the transaction are as follows:

- One of the most basic features of a transaction is that it must be measurable in terms of money in order to be classified as such.

- If any event brings any financial changes to the business organization, it will be considered as a transaction.

- There must be two parties in any transaction. In other words, one party will receive the benefit and the other will ensure that the same benefits are provided.

- Another essential characteristic of transactions is that each one is entirely distinct and indifferent to the others.

- Transactions may be seen or unseen.

- Historical transactions are financial transactions that occurred in the past.

- Any future events that affect the company’s financial status will be considered a transaction.

- Each transaction has an instant impact on the accounting equation.

you can also read: Short Questions and Answers-Transaction

“Every Event is not a Transaction but Every Transaction is an Event”

There are many events happening around us every day, but not all of them are recorded in the account books. Every transaction is created from one event but not all events are called transactions.

By analyzing the nature of the transaction, it is easy to understand which event is a transaction and which event is not a transaction.

Let’s try to find out why every event is not a transaction, but every transaction is an event.

The reason behind every event is not a transaction

- Basically, there are two types of events. Financial and non-financial. Events that change the financial position are called financial transactions, and events that do not change the financial position are called non-financial transactions.

- Every transaction has two sides, one side takes advantage of it and the other side provides benefits, i.e. the events in which the two parties are involved will be called a transaction and the rest will not be called a transaction.

- Events through which goods or services are exchanged are called transactions and through which goods or services are not exchanged are not called transactions.

- All events related to money or events that are measurable by the term of money are called transactions, but all other events not related to money are not called transactions.

- It is mandatory to have a document in a transaction, transactions that do not contain a document are not called transactions.

The reason behind every transaction is an event

- As a result of the transaction, financial and structural changes to the event are made, therefore, all transactions are one event.

- Every transaction changes the financial status of all events.

- Events that are self-sufficient and distinct are considered transactions.

- The events considered to be transactions are documented.

- Transactions may be both visible and invisible.

- There are two parties to each transaction, i.e. events that have two sides are considered transactions.

- Transactions in which goods and services are exchanged are considered to be transactions.

In view of the above, we can say that every event that happens every day in our business is not a transaction. But all of the transactions are events.

You may also read :

Classification of Transaction

Considering the nature of the transaction, the transaction can be divided into 5 categories, as follows:

Based on Objective:

i. Business Transactions:

Transactions that take place to run a business are called Business transactions.

Examples: buying-selling, income-expenditure-related transactions, etc.

ii. Non-Business Transactions:

Transactions that are not related to making a profit say non-business transactions.

Examples: Donations to hospitals, schools, colleges, and all these transactions of these institutions.

iii. Personal Transactions:

Money exchanged for personal, family food, clothing, shelter, education, entertainment is called personal transactions.

Examples: Buying furniture for the family, buying a TV, etc.

Based on Institution:

i. Internal Transactions:

Internal transactions are financial transactions that are not related to any external or third-party person or organization but are caused by the organization’s own policies and decisions are called internal transactions.

Examples: Depreciation, depletion, transfer from net profit to reserves, etc.

ii. External Transactions:

External Transactions are transactions that take place with any party outside the organization are called external transactions.

Examples: Buying and selling of goods, purchase of property, provision of services, salary, etc.

Based on the Monetary Term:

i. Cash Transactions:

A transaction performed in cash is called a cash transaction.

Examples: Buying and selling goods in cash, paying salaries in cash, buying property in cash, etc.

ii. Credit Transactions:

A credit transaction is the buying and selling of goods, services, and assets on credit.

Examples: Selling products on credit to Tanisha, purchasing a machine on credit from Tyra International, and so on.

iii. Non-Cash Transactions:

Non-cash transactions are transactions that have nothing to do with cash.

Examples: Depreciation, depletion, bad debts, discounts, etc.

Based on Visibility:

i. Visible Transactions:

Transactions that are visible with an open eye are called visible transactions.

Examples: Buildings, vehicles, machinery, furniture, etc.

ii. Invisible Transactions:

Transactions that are not visible with an open eye are called invisible or invisible transactions.

Examples: Depreciation of assets, depletion of leased assets, discounts on shares and debentures, Primary expenses, etc.

Based on Utility:

i. Capital Transactions:

Capital transactions are those that have long-term consequences. Capital transactions have a useful life of more than a year.

Examples: Purchase of furniture, purchase of equipment, etc.

ii. Revenue Transactions:

Revenue transactions are transactions that have a short-term outcome. A revenue transaction’s usefulness expires at the end of the fiscal year.

Examples: Rent, salary, electricity bill, etc.

How to Identify Transaction?

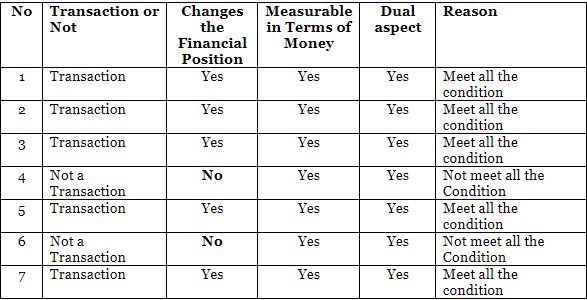

The following events will help us to identify which one is a transaction and which one is not a transaction:

- Started Business with $50,000

- Purchased Goods with cash $6,000

- Sold goods with cash $8,000

- Appointed Mark as a Manager with monthly salary $2,000

- Paid Monthly Rent with cash $4,000

- A contract signed to purchase goods from Nikita Enterprise worth $ 7000 Per Month.

- Sold goods to Brendon on credit $3,000

Now Identify Whether these events are a transaction or not.

- 6 accounting Principles

- Meaning of Accounting. Evolution of Accounting

- Accounting Ledger

- Accounting Journal

- Trial Balance

{kind=link}