Accounting Journal-Definition, Features, Rules for Journal Entry [Notes with PDF]

In this article, we will learn in-depth about the journal, including its definition, features, necessity or importance, format, preparation technique, and much more.

What is Journal?

There are numerous transactions taking place every day in every business organization. After that, the book on which these transactions are first recorded chronologically by means of a debit and credit analysis with proper explanation is called a journal.

Journal is a book containing a record of each day transactions.

Prof. Chambers

Journal is called the primary and subsidiary book of accounts.

Example of Journal:

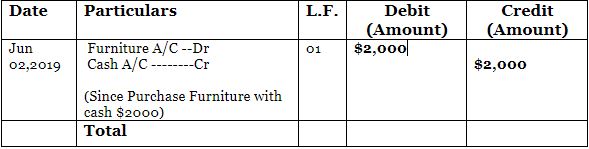

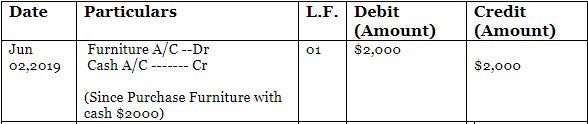

Mr. Nikon purchased a table for office on 21 July 2021 with cash of $4,000

How the transaction will be recorded in the Journal book is given below

Mr. Nikon’s Journal Book

| Date | Description | L.F. | Debit | Credit |

| 2021 | Furniture A/C | 4,000 | ||

| July, 21 | Cash A/C | 4,000 | ||

| (Since purchased a table for office with cash $4,000) |

8 Important Features or Nature of Journal

If we analyze the definition of a journal, we will find the following 8 important features of the Journal:

- Journal is the primary book of account.

- It is a daily book of accounts.

- Journal is an associate book of accounts.

- It records each transaction through a debit-credit analysis.

- It records each transaction with an explanation.

- Each transaction is recorded by means of a debit and credit analysis of the same amount of money in the journal.

- Journal is recorded in a specific table.

- The transaction is recorded in the Journal in a chronological manner.

Necessity or Importance of Journal

The importance of the Journal is immense. Basically, the process of accounting is started through the Journal.

The importance of the Journal is as follows:

- Journal is a permanent record of accounts.

- The nature of the transaction is known through Journal.

- Journalmaintains the continuity of the transaction.

- The transactions saved in Journal serve as future references.

- Journal acts as accounting information.

- It prevents fraud and cheats.

- Journal helps to resolve future disputes.

You can also read: Short Questions and Answers- Journal

Why Journal is called the subsidiary book of Accounts?

Journal is the daily, primary, and subsidiary book of accounts. That is, when a business transaction takes place, the book on which the first this transaction is recorded, with proper reason, is called Journal.

Journal is called the subsidiary book of accounts which serves as the basis for determining the final result in Accounting.

The following are the appropriate reasons for calling Journal a subsidiary book of accounts:

- Transactions are recorded first in Journal book then transferring those in Ledger, as a result, Ledger becomes easier.

- In the journal, transactions are recorded in a chronological manner in the future it can be used as proof of future evidence.

- In journal transactions are recorded with proper explanation, in the near future if any issue arises from the transaction, its explanation can be obtained from the journal.

- Journal ensures the accuracy of the Ledger.

- Transactions those transfers from Journal to Ledger do not need to be re-analyzed as a result, because the journal reduces the error and faults.

- Journal provides the idea of daily income and expenditure of the business.

You can also read the Difference between Journal and Ledger

Format of Journal

Journal Format: The journal format should have five columns.

- Date

- Particulars

- Ledger Folio

- Debit and

- Credit

Name of the Organization

Journal book

How to Prepare a Journal Entry or Rules for Journal Entry

1.Title Writing:

The name of the person or organization to be written in the journal book for which the journal book is being prepared.

Peter Enterprise’s

Journal Book

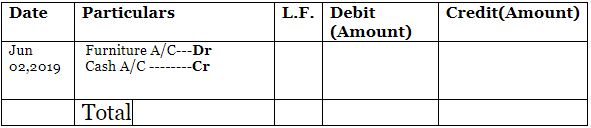

2. Date:

The transaction should be recorded chronologically in a journal book. The date in the journal book should be entered in the Date column.

3. Accounts Title:

After determining the account’s title of the transaction, it should be written to the particulars column analyzing debit and credit.

4. Debit and Credit:

The debit account (Dr.) should be entered in the first line and the credit account (Cr.) in the second line on the right.

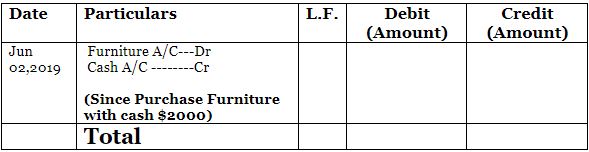

5. Transaction Explanation:

The reason for the transaction should be written in the bracket below after writing the debit and credit.

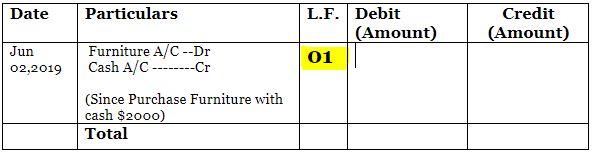

6. Ledger Folio Number:

The page number on which the account is recorded in Ledger will be shown here.

The amount of the debit and credit should be entered in the fourth and fifth columns of the journal. The sum of the debit and credit columns will always be equal.

Once the transaction is recorded, it must be closed by drawing a parallel line.

9. Closing Line:

At the end of the journal entries, two parallel lines should be drawn under the sum of each debit and the credit amount column.

you can also read:

| Journal Entries | Problem & Solution-01 | Problem & Solution-02 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}