Double Entry System of Accounting [Notes with PDF]

In this article, we will learn in-depth about the double-entry system, including its definition, examples, features, benefits or advantages, limitations or disadvantages, and much more.

What is the Double Entry System?

The best method of accounting in the current competitive world is the Double Entry System. It is known as a scientific and complete accounting system.

The double entry system is a system by which each transaction is measured in terms of money and expressed as a dual entity.

As well as the evolution of human civilization, Accounting has evolved. In ancient times, people used to keep their own accounts, but there have been many changes and developments in trade and trade over time, as well as many changes in the accounting method.

Especially during the industrial revolution, a period of change in the widespread expansion of business and in the process of production and distribution.

And this massive change led to the need for accountability in a scientific and acceptable way, and thus Luca Pacioli, the famous Italian mathematician, wrote in 1494 his famous book “Summa de Arithmetica, Geometria, Proportioniet Proportionlita” (“Collected Knowledge of Arithmetic, Geometry, Proportion, and Proportionality”).

Within his book, he described the ideal and proper reporting method for financial transactions, called the Double Entry System. And gradually, it has become the cornerstone of accounting.

The double-entry system is an accounting system where one party provides the benefit and the other party receives the benefit of each transaction. According to this method, there have been two or more accounts in each transaction. These accounts are written to the dual entity system. One is Debit and another is Credit.

According to this system, the total amount of the debit is always equal to the total amount of the credit.

What is The Examples of Double Entry System?

The examples of double-entry systems are as follows:

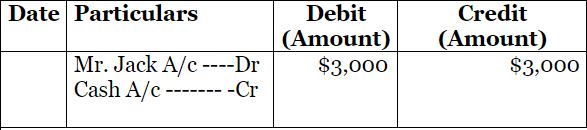

Paid cash $3,000 to Mr. Jack. If this transaction is recorded in the double-entry system, it will be as follows:

| Date | Particulars | Debit (Amount) | Credit (Amount) |

| Mr. Jack A/c—Dr. | $3,000 | ||

| Cash A/c——-Cr. | $3,000 |

What are the 6 Important Features or Principles of the Double Entry System?

The double-entry system is a modern and scientific accounting system. It is better than any other system of accounting.

The 6 important features or principles of this system are as follows:

- An important feature of this system is that each transaction has two sides-one is debit and the other is credit.

- There are one giver and one receiver in every transaction.

- The sum of the debit and the credit in each transaction is always equal.

- Each transaction is stored separately according to its classification, as it is stored in a double-entry system, which gives accurate results.

- It is a scientific method.

- Owners and companies are considered to be two separate artificial entities in the dual-entry system.

You can also read: Short Questions and Answers-Double Entry System

What are the 13 Important Advantages or Benefits of a Double Entry System?

It has undergone major changes in accounting. Since the invention of this method, accounting has been quite easy to manage and self-contained.

As a part of accounting, this system provides many benefits. The 13 important benefits or advantages of this system are as follows:

- It is a complete account of any transaction.

- The mathematical accuracy of the accounts can be verified by recording transactions.

- Determine the Profit and loss of a business organization easily.

- It provides accurate information on the actual financial condition of the business organization, such as income, expenditure, assets, and liabilities.

- It’s easy to get a sense of debt settlement.

- Accounting errors and frauds can be easily prevented.

- It serves as a formula for future planning.

- The management of the account in this manner is easily recognized globally.

- Control the additional costs of the organization

- Determine the price of the product.

- The organization can properly analyze its data and thus increase profits by recording transactions in this system.

- Determine the amount of VAT and income tax at the time of sales.

- This system is suitable for every small and large organization.

You can also read 3 Golden Rules of Accounting

What are the 6 Important Limitations or Disadvantages of Double Entry System?

Apart from the benefits of this system, there are some demerits or limitations, the nature of accounting in today’s competitive world has many complex shapes, and in some cases, there are difficulties in its implementation and circulation.

The 6 important limitations or disadvantages of this system are as follows:

- It is necessary for experienced people to keep an account in this method because this system can not be applied to the organization if there is no theoretical and practical knowledge of accounting, so making an account with inexperienced people can lead to many mistakes.

- It takes a lot of time and a lot of accounting books in the double-entry system, thus increasing the cost of the organization.

- Under this system, the accounting department records every transaction, which often leads to an error in the lack of skilled persons.

- This system can not record complete details of each accounting transaction because it keeps many accounting books in place.

- It analyzes the debit-credit of each transaction, but sometimes the debit-credit analysis creates complications that increase the number of errors.

- It is not easy to implement in small businesses. In this business, a single-entry system is more popular than a double-entry system to maintain accounts.

What Types of Books are Maintained under Double Entry System?

The types of books are maintained under the double-entry system are as follows:

1. Journal Book

- Purchase Book or Purchase Journal

- Sales Book or Sales Journal

- Purchase Return Book or Purchase Return Journal

- Sales Return Book or Sales Return Journal

- Book of Bills Receivable or Notes Receivable Journal

- Book of Bills Payable or Notes Payable Journal

- Journal in Proper or General Journal

- Cash Book

2. Ledger Book

1.Journal

Every day, the regular transactions of the business organization are written in this book, which is why it is called a journal.

Journal is called the primary book of accounts, Basic book of accounts, associate book of accounts, daily book of accounts, and so on.

To overcome the barriers of transaction form and recording, the journal can be divided into the following categories.

1.1. Purchase book or Purchase journal:

A purchasing book or purchase journal is the primary book of accounts that is used to record credit transactions of products purchased for the purpose of business or for sale. The Daily Purchase Book is another name for the Purchase Journal.

This book does not keep track of cash purchases of products. This book only records transactions concerning the purchasing of goods on credit.

1.2. Sales book or Sales Journal

The sales book or sales journal is the primary book of accounts used to record transactions concerning the credit selling of products. Daily Sales Book is another name for a sales journal.

This book does not record transactions involving the selling of products for cash. This book only records transactions concerning the selling of products on credit.

1.3. Purchase Return book or Purchase Return Journal

The purchase return book or purchase return journal is the book in which the transaction is recorded when goods purchased on credit are returned to the creditor.

Outward Return Book is another name for Purchase Return Journal.

1.4. Sales Return Book or Sales Return Journal

When the goods sold on credit are returned from the debtor, the book in which the transaction is recorded is called a sales return book or sales return journal.

Another name for this book is the Inward return book.

1.5. Books of Bills Receivable or Notes Receivable Journal

The bills receivable book or notes receivable journal is where the bill of money that is paid or accepted by the debtors is recorded.

1.6. Books of Bills Receivable or Notes Receivable Book

The bills payable book or Notes payable journal is where the bill is accepted in favor of the creditor is recorded.

1.7. Journal in Proper or General Journal

Transactions that cannot be included in any of the above categories are recorded in the journal in the proper or general journal.

1.8. Cashbook

A cash book is a book that records cash receipts and payments in a transaction. It doesn’t record any accrual transactions in this book.

Different forms of cash books exist. For example, the modern method keeps two journals for recording cash transactions: the Cash Receipt Journal and the Cash Payment Journal.

In addition, traditional methods are used for one-Column, two-column, three-column, multi-columns, and petty cash books.

2. Ledger

A ledger is a book of accounts that classifies and permanently records business transactions.

All entries in the other assistant books are classified and recorded permanently in the ledger, which is the main book of accounts.

I think you’ve learned all about the double-entry system. Don’t forget to comment on us if you have any confusion.

{kind=link}

Thanks a lot this helped me in my examination