Trial Balance- Definition, Features, Importance, Method [Notes with PDF]

In this article, we will learn in-depth about the trial balance, including its definition, features, importance, errors, methods of correcting errors, examples, and much more.

What is Trial Balance?

Trial Balance is a list of the balance of the accounts at a specific time.

Trial Balance is a list of the debit and credit balance of accounts derived from the Ledger at the end of the specified accounting period to check the mathematical accuracy of the accounts.

It checks the mathematical accuracy of the accounts to help the company prepare its financial statements.

That is, the trial balance is prepared to determine whether the Ledger accounts are correct or whether there is an error. In the Trial Balance, the balance of the debit column and the balance of the credit column is always equal.

Nature or Features of Trial Balance

Trial Balance is primarily designed to assist in the mathematical accuracy of accounts and to assist in the preparation of financial statements.

The important features of the trial balance are as follows:

- Trial balance is a list of ledger’s balances of accounts.

- It is easy to verify the mathematical accuracy of the Ledger Balance with the help of the Trial Balance.

- It is easier to prepare a final account or a financial statement on the basis of the trial balance.

- There is no obligation to create a Trial balance

- If there is an error in the accounts, it can be easily identified with the help of the Trial Balance.

- Trail balance is prepared at a convenient time at the end of the accounting period.

- Ledger balances of the accounts are recorded in the trial balance on a consecutive basis.

You can also read: Short questions and answers-Trial Balance

Necessity and the Importance of Trial Balance

The main purpose of the Trial balance is to verify the mathematical accuracy of the accounts It has many other objectives.

The importance or the necessity of the trial balance is as follows:

- It is very easy to verify the arithmetic accuracy of the accounts with the help of trial balance.

- Trial balance uncovers errors in the journaling and posting process.

- Trial Balance serves as an assistant in the preparation of financial statements.

- It is very easy to rectify if there are any inaccuracies in the accounts with the help of the trial balance.

- Trial balance provide the basic idea about the financial position of the company.

- As a result of the preparation of the trial balance, all accounts are available in one place, which does not require repeated checks on the account, saving both time and labor.

- It helps to make various comparisons among the accounts stored in the trial balance.

- Trial Balance plays an important role in the management analysis. Managers can easily take decisions based on the accounts information stored in the trial balance.

You may also read

Errors are Traced by the Trial Balance

The main purpose of the trial balance is to check the mathematical accuracy of the calculation.

The sum of the debit and credit balances of the account is always equal according to the Double-entry accounting method, If the sum of the two sides is not equal, the errors must be identified and the Trial Balance is prepared to identify and correct those errors.

Some of the errors traced by the trial balance are as follows:

1. Posting Errors

- Errors in Journalizing

- Errors in balancing of Ledger Account

- Errors in Partial Omission

2. Listing Errors

3. Costing and Balancing Errors

Errors are not Traced by the Trial Balance

The following are some of the errors that are not detected in the trial balance:

We can divide the errors that do not get traced in the trial balance

1. Critical Errors

- Errors of Omission

- Errors of Commission

- Errors of Miss posting

- Compensating Errors

Errors of Omission:

We know that when a transaction takes place, it is first recorded in the primary accounting book called the journal.

So if the transaction is not recorded in the Journal it will not belong to Ledger and the trial balance will not be reported.

As a result, the sum of the two sides of the trial balance will be equal, but this omission of the transaction can never be ascertained.

For example, if Neil was given a salary of $3000, it would never come to the trial balance if it was not accounted for, and it is an error of omission.

Errors of Commission:

If any transaction is recorded in the Journal by a lower or higher amount of money, the lower or higher amount will also be recorded in the Ledger and the trial balance will also be agreed upon.

For Example, Goods purchased from Wood International of $ 5000. If it is recorded in Purchase journal as $500 then both Purchase A/c and Wood International A/c will be lower valued by $4,500 and the trial balance will agree. These are the errors of commission.

Errors of Miss Posting:

Such errors are done because of the employee’s carelessness.

Suppose $ 3,000 has been paid in cash to “Kelley International”, Cashbook is correctly credited with $ 3,000 but while posting to the ledger Wood trader’s account is debited instead of “Kelley International”.

Trial Balance will match because the total of debits has been the same, though the amount has been credited to the wrong account.

Compensating Errors:

Compensating Errors is a type of error, that is when one wrong transaction is corrected by another wrong transaction, it is called a Compensating Errors.

Such as, Bony International A/c is supposed to be credited with $6,000 but it has been credited with $ 600. In another transaction, OWY international was debited with $ 600 by mistake instead of $ 6,000.

So both the accounts will be less by $ 5,400. In Spite of these errors, the Trial balance will match.

2. Errors of Principles

Errors that arise in the absence of proper knowledge of accounting principles are known as Principle Errors. This mistake occurred as a result of

When capital expenditure is recorded as revenue expenditure and revenue expenditure is recorded as capital expenditure.

For example,

Paid Machine installation charge for $300

Here wrongly debited “Repair and Maintenance Account” instead of “Machinery Account”

Furniture Purchase $ 5,000

Here wrongly debited “Purchase Account” instead of “Machinery Account”

In spite of the above errors in the trial balance, the debit and credit column balance of the trial balance will be matched

You can also read

Methods of Correcting an Incorrect Trial Balance

The steps that need to be taken to correct the incorrect Trial balance is discussed below:

- Check the sum of the Trial balance.

- Check that the posting from the journals to the Ledger account has been done correctly.

- Check that all balances of the ledger have been properly transferred to the Trial Balance.

- Check that Ledger’s debit and credit balances have been properly entered on the appropriate debit and credit side of the trial balance.

- The sum of the cash book should be checked.

- The sum of the list of debtors and creditors should be considered.

- The discrepancy between the two sides of the Trial Balance must be divided by 2 in order to see if there are any numbers that match the amount that is available by dividing by 2.

- Test whether the balances of assets, liabilities, and equity of the holder in the previous year have been correctly transferred to the Ledger account in the current year.

Upon proper examination, if any mistake is not identified, the amount by which the trial balance is incorrect should be entered for the time being in the Suspense Account.

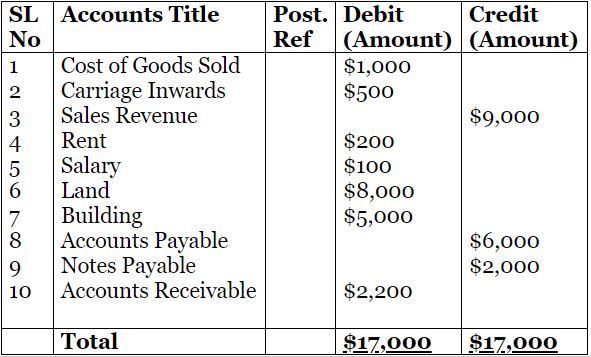

Format or Example of Trial Balance

The format or example of the trial balance is as follows:

Wood International

Trial Balance

For the year ended 30 June 2019

You May Also Like

- 10 Funny Accounting Jokes

- Advantages of Accounting Software

- Why Accounting is called The Language of Business

- Accrual Vs Cash Basis Accounting

{kind=link}

Thanks for sharing such an awesome blog on Trial balance and its features, format, and importance as well. This blog has useful information on Trial balance with examples and useful images. It helped a lot. Keep up the good work.

It’s awasome to have the insights blog from the Trial Balance perspective. It so helpful. The explanations examples given are straightforward making understanding so easy.

Thank you so much for the wonderful job well done.